Australia Wind Power Market Size, Share, Report 2025-2033

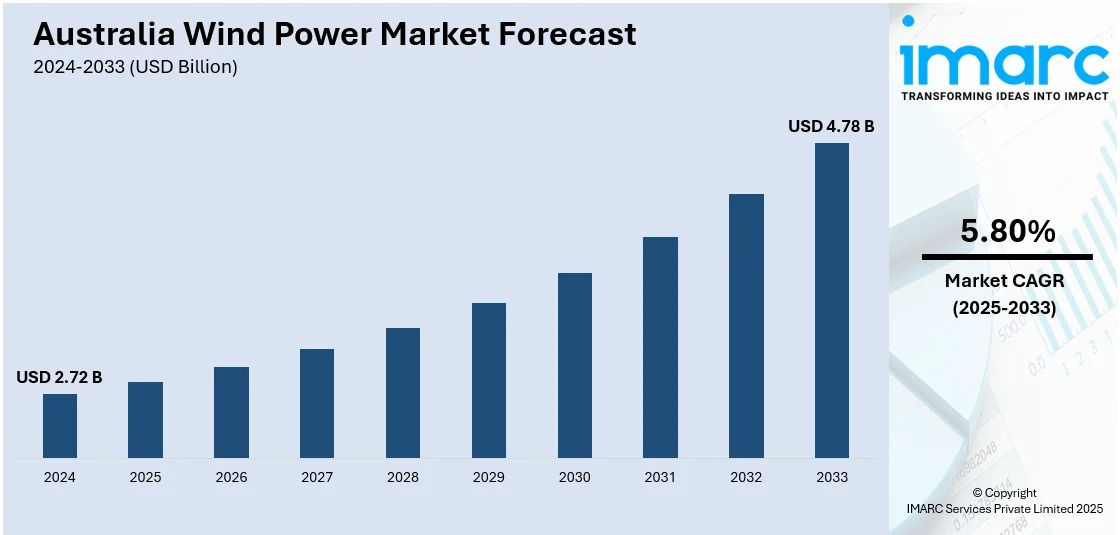

The Australia wind power market reached USD 2.72 Billion in 2024. Looking forward, IMARC Group expects the market to reach USD 4.78 Billion by 2033, exhibiting a growth rate (CAGR) of 5.80% during 2025-2033.

Australia Wind Power Market Overview

The Australia wind power market is experiencing robust expansion, driven by ambitious renewable energy targets, a massive onshore project pipeline, and the emergence of a transformative offshore wind sector. According to the latest report by IMARC Group, titled “Australia Wind Power Market: Industry Trends, Share, Size, Growth, Opportunity and Forecast 2026-2034,” the Australia wind power market reached USD 2.72 Billion in 2024. Looking forward, IMARC Group expects the market to reach USD 4.78 Billion by 2033, exhibiting a growth rate (CAGR) of 5.80% during 2025-2033.

Australia’s wind power industry spans both onshore and offshore installations, with a project pipeline exceeding 17.3 GW in various stages of development and 5.99 GW of projects actively under construction. The onshore segment dominates current installed capacity, with Australia approving 6.9 GW of onshore wind capacity in 2025 alone, while the offshore segment is emerging as a transformative growth frontier with Victoria setting targets of 2 GW by 2032, 4 GW by 2035, and 9 GW by 2040. The market is supported by a mature supply chain spanning turbine manufacturing, tower fabrication, foundation engineering, and balance-of-plant services, with cumulative energy storage capacity reaching 5,966 MWh by 2023 — including 2,603 MWh from utility-scale batteries — to complement wind generation variability.

The Australian wind power market is being propelled by several powerful converging factors. The national commitment to achieving 82% renewable electricity by 2030 under the Renewable Energy Target framework is creating strong policy tailwinds for wind investment. Corporate renewable energy procurement is accelerating, with over 1,700 MW of corporate power purchase agreements (PPAs) contracted in 2023 alone, providing revenue certainty that underpins project financing. Analysis released in March 2026 indicated that offshore wind development in Australia could reduce wholesale electricity prices by up to AUD 15/MWh by 2040, providing a compelling economic case for both onshore expansion and offshore investment. The progressive electrification of transport, industry, and heating is expanding total electricity demand, creating a structural need for additional generation capacity that wind energy is well-positioned to serve.

Request for a sample copy of this report: https://www.imarcgroup.com/australia-wind-power-market/requestsample

How AI is Reshaping the Future of the Australia Wind Power Market

Artificial intelligence is fundamentally transforming Australia’s wind power industry, enhancing energy output, reducing operational costs, and enabling more efficient integration of wind generation into the national electricity grid. From predictive wind forecasting that optimizes turbine performance to AI-driven maintenance platforms that minimize downtime across remote wind farm locations, these technologies are critical to realizing Australia’s ambitious renewable energy targets.

• Predictive Wind Forecasting and Generation Optimization: Machine learning models are analyzing meteorological data, historical wind patterns, and atmospheric conditions to produce highly accurate wind generation forecasts. These predictions enable Australian wind farm operators to optimize turbine yaw positioning, pitch angle, and rotational speed in real time, increasing annual energy production by 5-10% compared to conventional control strategies while reducing mechanical stress on turbine components.• AI-Powered Predictive Maintenance: Condition monitoring systems powered by machine learning are analyzing vibration, temperature, oil quality, and acoustic data from sensors embedded across turbine drivetrains, gearboxes, and generators to predict component failures weeks before they occur. This is particularly valuable for Australia’s geographically dispersed wind farms, where unplanned maintenance visits are expensive and time-consuming, enabling operators to schedule repairs during low-wind periods and minimize revenue losses.• Digital Twin Technology for Turbine Performance: AI-driven digital twins are creating virtual replicas of individual wind turbines and entire wind farms, enabling operators to simulate performance under various conditions, test control strategies, and optimize fleet-wide operations. These models continuously learn from real-world sensor data, identifying underperforming turbines and recommending targeted interventions that maximize output across Australia’s expanding wind fleet.• Intelligent Grid Integration and Dispatch: AI algorithms are optimizing the dispatch of wind-generated electricity into Australia’s National Electricity Market (NEM), analyzing real-time pricing signals, grid constraints, and demand forecasts to maximize revenue from wind generation. When paired with battery energy storage systems, AI-driven dispatch can store excess wind generation during low-price periods and release it during peak demand, improving the commercial returns of wind-storage hybrid projects.• AI-Assisted Site Selection for Offshore Wind: Machine learning is transforming offshore wind farm planning by analyzing complex datasets including wind resource assessments, seabed geotechnical surveys, environmental impact data, marine traffic patterns, and grid connection feasibility. As Australia progresses its offshore wind agenda — with Victoria’s first auction scheduled for August 2026 — AI-powered site optimization tools are helping developers identify locations that maximize energy yield while minimizing environmental and navigational impacts.

Australia Wind Power Market Trends

Emergence of Australia’s Offshore Wind Sector

The emergence of Australia’s offshore wind sector represents the most transformative trend reshaping the national wind power market. Victoria announced its first offshore wind auction scheduled for August 2026, targeting an initial 2 GW capacity tranche as the state works toward its ambitious 2 GW by 2032 and 9 GW by 2040 offshore wind targets. Star of the South — Australia’s most advanced offshore wind project — submitted its Environmental Impact Statement for approval, targeting construction later this decade to deliver up to 2.2 GW of generation capacity off the Gippsland coast. The Australian Government awarded final feasibility licenses to Bunbury Offshore Wind for two projects and to Westward Wind Pty Ltd in Western Australia, while Ørsted Offshore Australia secured a feasibility license for its Gippsland project, expected to be operational in the early 2030s. Analysis released in March 2026 indicated that offshore wind development could reduce wholesale electricity prices by up to AUD 15/MWh by 2040, providing a compelling economic rationale for large-scale offshore investment that complements Australia’s established onshore wind fleet.

Record-Scale Onshore Wind Farm Development

Australia’s onshore wind sector continues to set new records in project scale and development velocity. The 923 MW MacIntyre Wind Farm in Queensland’s Southern Downs region commenced full operations as Australia’s largest wind farm, featuring 162 turbines approximately 50 kilometers southwest of Warwick — a landmark project that demonstrates the industry’s capacity to deliver gigawatt-scale installations. The 412 MW Goyder South Wind Farm near Burra, South Australia, began operations in October 2025, estimated to generate approximately 1.5 TWh of renewable energy per year. The 400 MW Gawara Baya Wind Farm near Ingham, Queensland was approved for development and is set to power about 240,000 homes. With 6.9 GW of onshore wind capacity approved in 2025 and a total pipeline exceeding 17.3 GW, Australia’s onshore segment is experiencing unprecedented development momentum. The trend toward larger, more efficient turbines with higher hub heights and longer blade lengths is enabling wind farms to capture stronger, more consistent wind resources, improving capacity factors and reducing the levelized cost of energy.

Australia Wind Power Market Summary

• Market Size (2024): USD 2.72 Billion• Market Forecast (2033): USD 4.78 Billion• Growth Rate (CAGR 2025-2033): 5.80%• Key Segments: By Location (Onshore, Offshore)• Key Regions: Australia Capital Territory & New South Wales, Victoria & Tasmania, Queensland, Northern Territory & Southern Australia, Western Australia

Australia Wind Power Market Growth Drivers

Government Renewable Energy Targets and Policy Support

Australia’s ambitious government renewable energy targets — including the national goal of 82% renewable electricity by 2030 — are providing the foundational policy framework driving wind power investment. State-level targets and incentives are complementing federal ambitions, with Victoria’s dedicated offshore wind targets of 2 GW by 2032 and 9 GW by 2040 creating a clear regulatory pathway for project development and investment certainty. The Offshore Electricity Infrastructure Act and associated regulatory frameworks provide the legal foundation for offshore wind development, while Renewable Energy Zones (REZs) designated across New South Wales, Queensland, and other states are streamlining grid connection approvals and coordinating transmission infrastructure investment to support wind farm development. These policy frameworks reduce investment risk and attract both domestic and international capital, creating a virtuous cycle of investment, deployment, and cost reduction that sustains market growth across both onshore and offshore segments.

Corporate PPA Growth and Revenue Certainty

The rapid expansion of corporate renewable energy procurement is emerging as a critical growth driver for Australia’s wind power market. With over 1,700 MW of corporate power purchase agreements contracted in 2023 alone, large energy consumers — including major technology companies, mining operators, manufacturers, and retailers — are securing long-term wind energy contracts that provide the revenue certainty needed to underpin project financing and construction. Corporate PPAs are increasingly sophisticated, with multi-buyer structures, firming arrangements, and green certification features that create attractive commercial propositions for both wind developers and off-takers. This demand-side pull is particularly powerful because it operates independently of government subsidy cycles, creating market-driven investment signals that attract private capital and support project pipeline development. The growing corporate focus on Scope 2 emissions reduction targets under ESG reporting frameworks is further expanding the pool of potential PPA buyers, sustaining demand growth for wind-generated electricity.

Australia Wind Power Market Segments

The Australia wind power market can be segmented across key dimensions. By location, the market includes onshore and offshore installations. Onshore wind dominates current installed capacity with a pipeline exceeding 17.3 GW and 6.9 GW approved in 2025, while offshore wind is emerging as the next major growth frontier with Victoria targeting 9 GW by 2040 and multiple feasibility licenses granted across Gippsland and Western Australia. By region, the market spans Australia Capital Territory & New South Wales, Victoria & Tasmania, Queensland, Northern Territory & Southern Australia, and Western Australia. Queensland is leading large-scale onshore development with projects including the 923 MW MacIntyre Wind Farm, while Victoria & Tasmania is pioneering offshore wind through dedicated state targets and the Star of the South project. South Australia continues as a wind energy leader with projects like the 412 MW Goyder South Wind Farm, while Western Australia is advancing offshore feasibility with licensed projects off Bunbury.

Breakup by Location:

• Onshore• Offshore

Breakup by Region:

• Australia Capital Territory & New South Wales• Victoria & Tasmania• Queensland• Northern Territory & Southern Australia• Western Australia

Australia Wind Power Market Competitive Landscape

The competitive landscape of the Australia wind power market features a mix of international energy developers, turbine manufacturers, and domestic renewable energy companies. Key players in the market include Acciona S.A., APA Group, Ark Energy Corporation, Goldwind Science & Technology, Iberdrola S.A., Neoen Australia, RATCH Australia Corporation, Suzlon Energy Australia, Tilt Renewables, Vestas Wind Systems, and WestWind Energy. Acciona delivered the landmark 923 MW MacIntyre Wind Farm using Goldwind turbines, demonstrating capability in gigawatt-scale project execution. Vestas Wind Systems maintains a strong position as a leading turbine supplier across multiple Australian projects. Neoen Australia is a prominent independent power producer with a growing portfolio of onshore wind and hybrid projects. In the emerging offshore segment, Star of the South (backed by Copenhagen Infrastructure Partners) leads development with its 2.2 GW Gippsland project, while Ørsted and Bunbury Offshore Wind have secured feasibility licenses for projects across Victoria and Western Australia.

Australia Wind Power Market Latest News and Development

• August 2026 (Upcoming): Victoria announced its first offshore wind auction targeting an initial 2 GW capacity tranche, marking a historic milestone in Australia’s offshore wind development as the state works toward its 2 GW by 2032, 4 GW by 2035, and 9 GW by 2040 offshore wind targets.• 2025: The 923 MW MacIntyre Wind Farm in Queensland’s Southern Downs region commenced full operations as Australia’s largest wind farm, featuring 162 Goldwind turbines. The project represents a landmark achievement in gigawatt-scale onshore wind development in Australia.• October 2025: The 412 MW Goyder South Wind Farm near Burra, South Australia, began operations, estimated to generate approximately 1.5 TWh of renewable energy per year, reinforcing South Australia’s position as a leading wind energy state.• 2025: Star of the South, Australia’s most advanced offshore wind project, submitted its Environmental Impact Statement for approval, targeting construction later this decade to deliver up to 2.2 GW of generation capacity off the Gippsland coast in Victoria.• 2025: The Australian Government awarded final feasibility licenses to Bunbury Offshore Wind for two projects and to Westward Wind in Western Australia. Ørsted Offshore Australia also secured a feasibility license for its Gippsland project, expected to be operational in the early 2030s. Australia approved 6.9 GW of onshore wind capacity during the year.

Note: If you require any specific information not currently covered within the scope of the report, IMARC Group will provide it as part of customization.

Speak to an analyst:

https://www.imarcgroup.com/request?type=report&id=33748&flag=E

𝗔𝗯𝗼𝘂𝘁 𝗨𝘀

IMARC Group is a global management consulting firm that helps companies in strategy, operations, technology, and innovation. We have a strong track record of providing comprehensive market research reports and advisory services to a broad range of clients, including Fortune 500 companies, governments, and startups. Our reports cover over 3,000 markets across various industry verticals, providing in-depth analysis and insights on market size, share, growth, trends, and forecasts.

𝗖𝗼𝗻𝘁𝗮𝗰𝘁 𝗨𝘀

IMARC Group

134 N 4th St. Brooklyn, NY 11249, USA

Email: sales@imarcgroup.com

Tel No: (D) +91 120 433 0800

United States: +1-631-791-1145