Australia Logistics Market Size, Share, Report 2026-2034

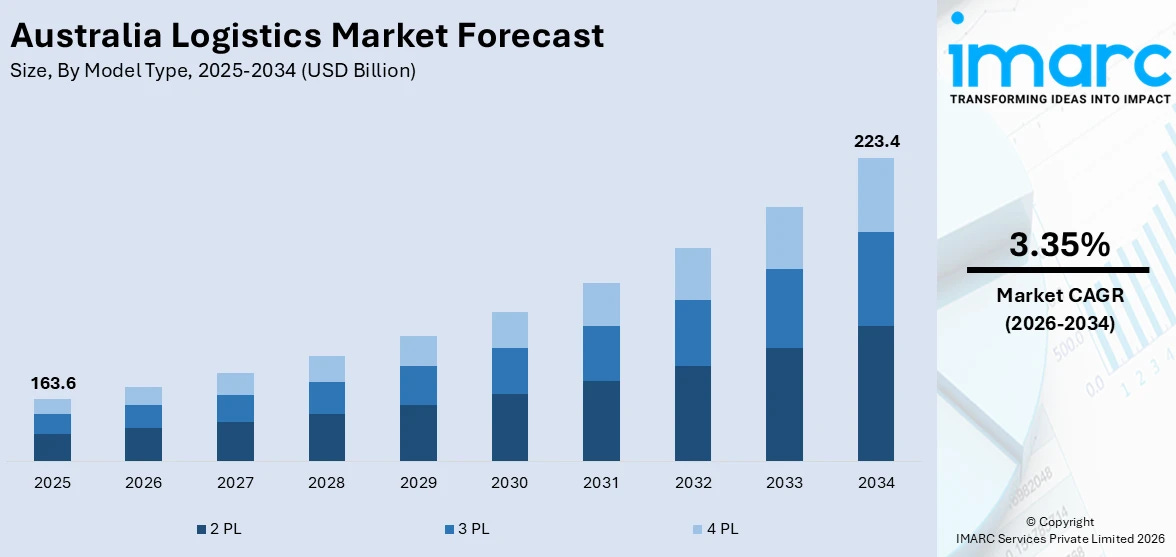

Australia logistics market size reached USD 163.6 Billion in 2025. Looking forward, the market is expected to reach USD 223.4 Billion by 2034, exhibiting a growth rate (CAGR) of 3.35% during 2026-2034.

Australia Logistics Market Overview

The Australia logistics market is experiencing sustained growth, driven by the convergence of expanding e-commerce volumes, large-scale government infrastructure investment, accelerating fleet electrification, deepening supply chain digitalisation, and the strategic importance of Australia’s position as a major commodity exporter and Asia-Pacific trade gateway. The Australia logistics market size reached USD 163.6 Billion in 2025, reflecting the structural significance of logistics in supporting Australia’s USD 1.7 trillion economy across manufacturing, mining, agriculture, retail, and healthcare sectors. Road freight retained a dominant 67.10% revenue share in 2025, underscoring the critical role of trucking networks in connecting Australia’s geographically dispersed population centres and industrial hubs. E-commerce parcel traffic grew 15% in 2024, prompting Australia Post to extend same-day delivery coverage to 85% of Sydney and Melbourne postcodes, while 35% of Australian SMEs deployed AI-enabled logistics solutions in 2024, achieving average cost savings of 18% and lead-time reductions of 22%.

Looking forward, the Australia logistics market is expected to reach USD 223.4 Billion by 2034, exhibiting a growth rate (CAGR) of 3.35% during 2026-2034. This growth trajectory is being underpinned by transformative infrastructure investments, fleet electrification at unprecedented scale, and the rapid integration of automation and artificial intelligence across the logistics value chain. Linfox ordered 200 Volvo electric trucks in October 2024 — the nation’s largest single commercial EV deal — with charging hubs planned across five capital cities, while in May 2025 Volvo confirmed the largest electric truck order in Australia with 30 battery-electric heavy-duty units for Linfox. Team Global Express announced plans to incorporate more than 300 electric trucks, vans, and mobile chargers into its fleet, backed by a AUD 190 million financing agreement led by the Clean Energy Finance Corporation. The Australia logistics automation market reached USD 1,818.8 million in 2025 and is projected to reach USD 4,370.7 million by 2034 at a CAGR of 10.23%, with DHL Supply Chain deploying approximately 1,000 assisted picking robots across Australian warehouses. ARENA provided Toll and Linfox with a shared AUD 28.6 million in electrification funding, while Toll Group completed its USD 200 million electric-vehicle rollout in December 2024, adding 500 battery trucks and AI telematics to metropolitan fleets. The convergence of sustainability mandates, technology adoption, and capacity expansion is reshaping Australia’s logistics landscape from a cost-centre model into a strategic competitive differentiator.

Request for a sample copy of this report: https://www.imarcgroup.com/australia-logistics-market/requestsample

How AI is Reshaping the Future of the Australia Logistics Market

Artificial intelligence is fundamentally transforming Australia’s logistics industry, driving efficiency gains across warehouse operations, freight management, supply chain visibility, fleet optimisation, and demand forecasting. As the industry moves from manual, experience-based decision-making toward data-driven, autonomous operations, AI is unlocking productivity improvements that were previously unattainable. Key developments include:

• AI-Powered Warehouse Automation and Robotic Fulfilment: Machine learning algorithms integrated with autonomous mobile robots (AMRs) and collaborative robots (cobots) are revolutionising Australian warehouse operations, handling picking, packing, and material transport with increasing sophistication. DHL Supply Chain is deploying approximately 1,000 assisted picking robots across its Australian warehouses, while early 2025 data confirms that SMEs adopting cobots in food processing operations are achieving 50% operational efficiency gains. These robotics systems are expected to reduce logistics costs by up to 40% and boost productivity by 25% to 70%, with AI enabling adaptive learning that allows robots to optimise their movements based on real-time warehouse conditions and order patterns.

• Predictive Supply Chain Analytics and Demand Forecasting: Machine learning models are analysing vast datasets encompassing historical shipment volumes, seasonal patterns, macroeconomic indicators, weather forecasts, and consumer behaviour signals to deliver increasingly accurate demand predictions that optimise inventory positioning and resource allocation. With 35% of Australian SMEs deploying AI-enabled logistics solutions in 2024 and achieving average cost savings of 18% and lead-time reductions of 22%, predictive analytics is demonstrating measurable ROI across businesses of all sizes, enabling proactive rather than reactive supply chain management.

• AI-Optimised Fleet Management and Route Intelligence: AI-driven fleet management platforms are transforming freight transportation by combining real-time GPS tracking, traffic analytics, weather data, and vehicle telemetry to optimise routing, fuel consumption, and driver scheduling across Australia’s vast road freight network. Toll Group’s integration of AI telematics into its metropolitan fleet of 500 battery trucks enables real-time performance monitoring, predictive maintenance scheduling, and dynamic route adjustment that maximises both operational efficiency and electric vehicle range utilisation across diverse delivery conditions.

• Digital Twin and IoT-Enabled Supply Chain Visibility: Australian logistics operators are deploying IoT sensors integrated with AI-driven analytics platforms to create digital twins of their supply chain networks, enabling real-time visibility across warehousing, transportation, and last-mile delivery operations. These systems provide end-to-end tracking, environmental condition monitoring for temperature-sensitive goods, and automated exception management that identifies and resolves disruptions before they impact delivery commitments, supporting the growth of the temperature-controlled warehousing segment which is expanding at a 4.10% CAGR.

• AI-Driven Sustainability Optimisation and Carbon Accounting: AI platforms are enabling Australian logistics companies to quantify, optimise, and report their carbon emissions with scientific precision, supporting corporate sustainability targets and regulatory compliance. Machine learning algorithms optimise load consolidation, modal selection, and routing decisions to minimise carbon intensity per tonne-kilometre, while AI-powered carbon accounting systems provide granular emissions data across Scope 1, 2, and 3 categories that meet emerging ESG reporting requirements and support the transition toward net-zero logistics operations.

Australia Logistics Market Trends

Fleet Electrification Accelerating at Unprecedented Scale Across Australian Logistics Networks

The electrification of logistics fleets has emerged as the most transformative trend reshaping Australia’s logistics landscape, with major operators committing to large-scale electric vehicle deployments backed by substantial government funding, private capital investment, and strategic manufacturing partnerships. Linfox — Australia’s largest privately owned logistics company — ordered 200 Volvo electric trucks in October 2024, representing the nation’s largest single commercial EV deal, with charging hubs planned across five capital cities. In May 2025, Volvo confirmed a further order of 30 battery-electric heavy-duty trucks (29 FH Electric and 1 FM Electric) for Linfox, marking the largest electric truck order in Australian history, with some units to be assembled at Volvo’s Wacol facility in Brisbane during 2026 — signalling the emergence of domestic EV truck assembly capability. Team Global Express announced plans to incorporate more than 300 electric trucks, vans, and mobile chargers into its fleet, supported by a AUD 190 million financing agreement led by the Clean Energy Finance Corporation. Toll Group completed its USD 200 million electric-vehicle rollout in December 2024, adding 500 battery trucks and AI telematics to metropolitan fleets, while its Project TruckVolt initiative — supported by up to AUD 9 million in ARENA funding — is deploying 28 battery-electric trucks including 10 Volvo FM Electric prime movers and 18 Volvo FE Electric rigids. ARENA provided Toll and Linfox with a shared AUD 28.6 million in electrification funding, with Linfox receiving AUD 19.6 million to deploy 26 battery-electric trucks and charging infrastructure across three distribution centres in Queensland, South Australia, and Victoria. This rapid fleet electrification is driven by the convergence of tightening emissions regulations, declining battery costs, improving vehicle range and payload capabilities, and growing customer demand for low-carbon freight services across retail, FMCG, and pharmaceutical supply chains.

Logistics Automation and Robotics Investment Transforming Warehouse and Distribution Operations

The rapid acceleration of automation and robotics investment across Australian warehousing and distribution operations represents a structural shift in the logistics industry, driven by labour shortages, rising wage costs, e-commerce volume growth, and the proven ROI of AI-powered automation solutions. The Australia logistics automation market reached USD 1,818.8 million in 2025 and is projected to reach USD 4,370.7 million by 2034, growing at a CAGR of 10.23%, reflecting the scale of technology investment flowing into the sector. The Australian industrial robotics market is projected to reach USD 1.85 billion by 2033, growing at 12.8% annually, while logistics-specific automation is expected to expand at an even more aggressive 13.9% CAGR. DHL Supply Chain’s deployment of approximately 1,000 assisted picking robots across Australian warehouses represents major confidence in automation maturity, while autonomous mobile robots (AMRs) are replacing traditional fixed conveyor systems with flexible, AI-guided material handling that adapts to changing warehouse layouts and order profiles. Collaborative robots (cobots) are democratising automation for SMEs by eliminating the need for expensive safety infrastructure — early 2025 data confirms that food processing SMEs adopting cobots are achieving 50% operational efficiency gains. Amazon has unveiled next-generation warehouse AI and robotics technologies with Australia firmly on its deployment radar, signalling the competitive pressure driving automation adoption across the industry. Non-temperature controlled warehouses dominate with a 91.60% revenue share in 2025, but temperature-controlled space is the fastest-growing segment at a 4.10% CAGR driven by vaccine distribution and fresh food export requirements that demand precise automated climate management. The convergence of robotics with AI-driven inventory management, computer vision quality control, and predictive maintenance systems is creating intelligent warehouses that operate with significantly higher throughput, accuracy, and energy efficiency than traditional manual operations.

Australia Logistics Market Summary

• The Australia logistics market reached USD 163.6 Billion in 2025 and is projected to reach USD 223.4 Billion by 2034 at a CAGR of 3.35%, driven by e-commerce growth, infrastructure investment, fleet electrification, and automation adoption across the supply chain.

• Road freight retained a 67.10% revenue share in 2025, while e-commerce parcel traffic grew 15% in 2024, prompting Australia Post to extend same-day delivery coverage to 85% of Sydney and Melbourne postcodes.

• Linfox ordered 200 Volvo electric trucks in October 2024 — the nation’s largest single commercial EV deal — while Team Global Express committed to 300+ electric vehicles backed by AUD 190 million CEFC financing.

• The logistics automation market reached USD 1,818.8 million in 2025, projected to grow to USD 4,370.7 million by 2034 at a 10.23% CAGR, with DHL Supply Chain deploying 1,000 assisted picking robots across Australian warehouses.

• 35% of Australian SMEs deployed AI-enabled logistics solutions in 2024, achieving average cost savings of 18% and lead-time reductions of 22%, while robotics are expected to reduce logistics costs by up to 40% and boost productivity by 25-70%.

Australia Logistics Market Growth Drivers

E-Commerce Expansion and Omnichannel Retail Fulfilment Driving Logistics Demand

Australia’s rapidly expanding e-commerce sector is the primary structural driver of logistics market growth, generating sustained increases in parcel volumes, warehousing demand, last-mile delivery requirements, and reverse logistics complexity that are transforming the scale and sophistication of logistics operations across the country. E-commerce parcel traffic grew 15% in 2024, reflecting the structural shift in Australian consumer purchasing behaviour toward online channels that is now well established and accelerating. Australia Post extended same-day delivery coverage to 85% of Sydney and Melbourne postcodes in response to rising consumer expectations for speed and convenience, while its planned USD 500 million AI-powered mega parcel hub at the former Holden site in Elizabeth, South Australia, with capacity for 400,000 parcels per day, represents the industry’s largest single infrastructure investment to meet projected e-commerce growth. The wholesale and retail trade segment — particularly e-commerce — dominates logistics demand, driving expansion across warehousing, transportation, and fulfilment services. The proliferation of omnichannel retail models — integrating online ordering, in-store pickup, same-day delivery, and returns processing — is creating multi-modal logistics complexity that requires sophisticated technology platforms, flexible warehouse configurations, and dynamic fleet management capabilities. Third-party logistics (3PL) providers are experiencing particularly strong growth as retailers increasingly outsource fulfilment operations to specialists with the technology infrastructure and network scale to deliver competitive service levels. The growth of cross-border e-commerce, social commerce, and marketplace platforms is adding international logistics demand to the domestic growth trajectory, expanding opportunities across air freight, customs brokerage, and international parcel services.

Government Infrastructure Investment and Sustainability Mandates Enabling Capacity Expansion

The convergence of large-scale government infrastructure investment and tightening sustainability regulations is creating a powerful dual catalyst for logistics market growth by simultaneously expanding physical network capacity and driving technology-led operational transformation. The Australian Government’s commitment to major transport infrastructure programs is improving road, rail, and port connectivity that directly reduces freight transit times, lowers transportation costs, and extends the geographic reach of efficient logistics services across Australia’s vast territory. These infrastructure investments are particularly impactful for connecting regional and remote areas to metropolitan logistics hubs, addressing the cost and efficiency challenges that arise from Australia’s unique geography of concentrated coastal populations separated by vast distances. Simultaneously, government sustainability mandates and funding programs are accelerating the logistics industry’s transition toward electric fleets, renewable energy-powered warehouses, and carbon-neutral operations. ARENA’s AUD 28.6 million in electrification funding shared between Toll and Linfox, combined with the Clean Energy Finance Corporation’s AUD 190 million financing for Team Global Express, demonstrates the scale of public financial support for logistics decarbonisation. Volvo’s announcement to begin electric truck production at its Wacol facility in Brisbane during 2026 marks the emergence of domestic EV truck manufacturing capability that will reduce lead times and support the industry’s electrification trajectory. The regulatory environment is also driving growth in the 4PL segment, where lead logistics providers manage complex, multi-modal supply chains on behalf of clients to meet sustainability reporting requirements, carbon reduction targets, and circular economy obligations that extend across Scope 1, 2, and 3 emissions. These combined infrastructure and sustainability drivers are expanding the total addressable market for logistics services by creating demand for higher-value, technology-enabled, and environmentally compliant solutions that command premium pricing compared to traditional commodity freight services.

Australia Logistics Market Segments

The Australia logistics market is comprehensively segmented across model type, transportation mode, end use sector, and region, providing a detailed framework for analysing growth opportunities and competitive dynamics across the logistics value chain.

• Breakup by Model Type: The market is segmented into 2PL, 3PL, and 4PL logistics models. The 3PL segment represents the largest and fastest-growing category as retailers, manufacturers, and e-commerce businesses increasingly outsource warehousing, transportation, and fulfilment operations to specialist providers with the technology infrastructure, network scale, and operational expertise to deliver competitive service levels and cost efficiencies.

• Breakup by Transportation Mode: The market encompasses roadways, seaways, railways, and airways. Road freight dominates with a 67.10% revenue share in 2025 due to its door-to-door versatility across Australia’s dispersed settlements, while railways serve bulk commodity and intermodal freight corridors, seaways handle international trade and coastal shipping, and airways support time-critical express deliveries and high-value cargo.

• Breakup by End Use: The market serves manufacturing, consumer goods, retail, food and beverages, IT hardware, healthcare, chemicals, construction, automotive, telecom, oil and gas, and other sectors. The retail and consumer goods segments are experiencing the strongest growth driven by e-commerce expansion, while healthcare logistics is gaining momentum from vaccine distribution, cold chain requirements, and pharmaceutical supply chain complexity.

• Breakup by Warehousing: Non-temperature controlled warehouses dominate with a 91.60% revenue share in 2025, while temperature-controlled facilities represent the fastest-growing segment at a 4.10% CAGR driven by expanding vaccine distribution networks, fresh food exports, pharmaceutical storage requirements, and the growing cold chain demands of online grocery delivery services.

• Breakup by Region: The market is segmented across Australian Capital Territory & New South Wales, Victoria & Tasmania, Queensland, Northern Territory & Southern Australia, and Western Australia. New South Wales and Victoria lead in logistics activity driven by the concentration of major ports, distribution centres, and consumer markets in Sydney and Melbourne, while Queensland and Western Australia serve critical mining, agriculture, and resource export logistics corridors.

Australia Logistics Market Competitive Landscape

The Australia logistics market features a competitive landscape comprising major domestic operators, global logistics corporations, and specialist freight and fulfilment providers. Key players operating in the market include Aurizon Ltd., Centurion Transport, DB Schenker, DHL Group, DSV A/S, FedEx Corporation, K&S Group, Kuehne+Nagel International AG, Linfox Pty Ltd., Qube Holdings Ltd., Toll Group (Japan Post Holdings), Team Global Express, Australia Post, and StarTrack, among others. These companies compete through network scale, technology capabilities, fleet modernisation, sustainability credentials, and industry-specific logistics expertise to serve Australia’s diverse freight and supply chain requirements.

Latest News & Development in the Australia Logistics Market

• May 2025: Volvo Trucks received an order for 30 battery-electric heavy-duty trucks from Linfox — 29 FH Electric and 1 FM Electric — marking the largest electric truck order in Australia, with some units to be assembled at Volvo’s Wacol facility in Brisbane during 2026.

• December 2024: Toll Group completed its USD 200 million electric-vehicle rollout, adding 500 battery trucks and AI telematics to its metropolitan fleet operations across major Australian cities.

• November 2024: ARENA provided Toll and Linfox with a shared AUD 28.6 million in electrification funding — Linfox received AUD 19.6 million to deploy 26 battery-electric trucks across Queensland, South Australia, and Victoria, while Toll received up to AUD 9 million for its AUD 67 million Project TruckVolt deploying 28 battery-electric trucks.

• October 2024: Linfox ordered 200 Volvo electric trucks — the nation’s largest single commercial EV deal — with charging hubs planned across five capital cities, marking a transformative milestone in Australian logistics fleet electrification.• 2025: Team Global Express announced plans to incorporate more than 300 electric trucks, vans, and mobile chargers into its fleet, supported by a AUD 190 million financing agreement led by the Clean Energy Finance Corporation to accelerate logistics decarbonisation.

Note: If you require any specific information not currently covered within the scope of the report, IMARC Group will provide it as part of customization.

Speak to an analyst:

https://www.imarcgroup.com/request?type=report&id=21952&flag=E

𝗔𝗯𝗼𝘂𝘁 𝗨𝘀

IMARC Group is a global management consulting firm that helps companies in diverse industries achieve sustainable growth through data-driven insights, strategic advisory, and cutting-edge research. Our extensive portfolio of market research reports spans across multiple sectors, providing actionable intelligence that empowers businesses to make informed decisions, identify growth opportunities, and stay ahead of the competition. From healthcare and technology to consumer goods and heavy industry, IMARC’s research capabilities cover a wide spectrum of markets, enabling clients across the globe to navigate complex market dynamics, capitalize on emerging trends, and drive long-term value creation.

𝗖𝗼𝗻𝘁𝗮𝗰𝘁 𝗨𝘀

IMARC Group

134 N 4th St. Brooklyn, NY 11249, USA

Email: sales@imarcgroup.com

Tel No: (D) +91 120 433 0800

United States: +1-631-791-1145