Australia Fertilizer Market 2026 | Worth USD 3.9 Billion by 2034

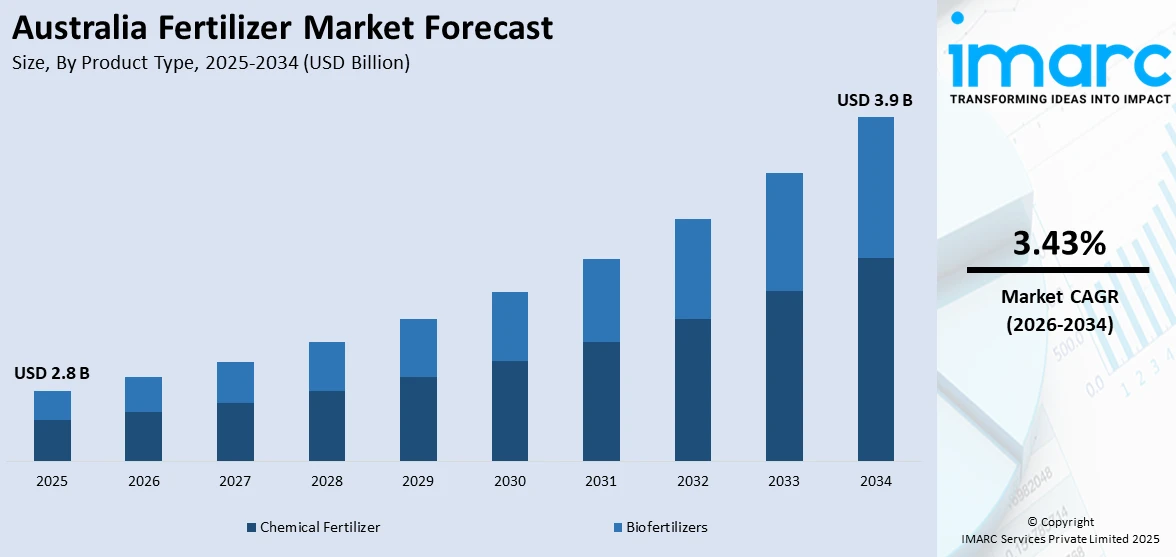

Australia fertilizer market size reached USD 2.8 Billion in 2025. Looking forward, the market is expected to reach USD 3.9 Billion by 2034, exhibiting a growth rate (CAGR) of 3.43% during 2026-2034.

Australia Fertilizer Market Overview

The Australia fertilizer market is experiencing steady growth, underpinned by rising agricultural productivity demands, expanding adoption of precision farming technologies, and a national push toward food security. As one of the world's leading agricultural exporters—with farm exports reaching approximately USD 46 billion in fiscal year 2023-24—the country's reliance on both chemical and biological fertilizers continues to deepen. The Australia fertilizer market size reached USD 2.8 Billion in 2025. Looking forward, IMARC Group expects the market to reach USD 3.9 Billion by 2034, exhibiting a growth rate (CAGR) of 3.43% during 2026-2034. Nitrogenous fertilizers, including urea, calcium ammonium nitrate, and anhydrous ammonia, remain fundamental to broad-acre cropping across wheat, canola, and barley regions, while phosphatic formulations such as MAP and DAP support root development in grain and horticultural systems.

Australia's fertilizer consumption landscape is shaped by the country's diverse climatic zones, soil types, and crop rotations. Western Australia and New South Wales dominate cereal production and accordingly account for a significant share of nitrogenous and phosphatic fertilizer usage, while Queensland and Victoria lead in horticultural and specialty crop applications that increasingly rely on micronutrient and liquid fertilizer formulations. The market encompasses both straight fertilizers—including nitrogenous, phosphatic, potash, secondary macronutrient, and micronutrient categories—and complex blended products tailored to specific soil-crop combinations. With straight blends holding an estimated 86.9% of the market in 2025, broad-acre efficiency continues to drive bulk fertilizer demand. Meanwhile, the biofertilizer segment is gaining traction as sustainable farming practices expand across organic and regenerative agricultural operations nationwide.

How AI is Reshaping the Future of the Australia Fertilizer Market

Artificial intelligence is fundamentally transforming how fertilizers are manufactured, distributed, and applied across Australian agriculture. From predictive analytics that optimize nutrient delivery to autonomous systems that reduce waste and environmental impact, AI-driven innovations are reshaping every link of the fertilizer value chain.

• Precision Nutrient Management: AI-powered variable-rate application (VRA) systems, now adopted by more than half of Australian farmers, analyze real-time soil sensor data, satellite imagery, and weather forecasts to prescribe zone-specific fertilizer rates. These systems have demonstrated a projected 15% reduction in fertilizer usage while maintaining or improving crop yields, delivering significant cost savings and reducing nutrient runoff into waterways.

• Drone-Based Aerial Monitoring and Application: AI-equipped agricultural drones using GPS, LiDAR, and computer vision technologies are enabling farmers to conduct high-resolution crop health assessments and targeted fertilizer application. These systems identify nutrient-deficient zones with centimeter-level accuracy, allowing micro-targeted delivery of liquid and granular fertilizers that minimize waste and environmental contamination across vast pastoral and cropping landscapes.

• Predictive Soil Analytics and Digital Twin Models: Machine learning algorithms are processing decades of soil composition data alongside real-time moisture, pH, and organic matter readings to build digital twin models of Australian farmland. These predictive platforms forecast nutrient depletion cycles and recommend proactive fertilization schedules, helping growers transition from reactive to anticipatory soil management and improving long-term soil health across grain belts and horticultural regions.

• Autonomous Fertilizer Spreading Equipment: AI-guided autonomous tractors and spreaders are being deployed across large-scale Australian farms to execute fertilizer application with consistent precision around the clock. These self-navigating machines integrate real-time data feeds from soil sensors and crop monitoring systems, adjusting application rates dynamically and operating in conditions where manual labor is impractical, addressing both labor shortages and operational efficiency challenges in remote farming regions.

• AI-Optimized Supply Chain and Demand Forecasting: Artificial intelligence models are being deployed by fertilizer manufacturers and distributors to predict seasonal demand fluctuations, optimize inventory management, and streamline logistics networks across Australia's vast geography. By analyzing historical purchasing patterns, weather outlooks, commodity prices, and crop planting intentions, these systems reduce stockout risks, minimize storage costs, and ensure timely fertilizer availability during critical planting windows.

Request a Business Sample Report for Procurement & Investment Evaluation: https://www.imarcgroup.com/australia-fertilizer-market/requestsample

Australia Fertilizer Market Trends

Shift Toward Domestic Fertilizer Production and Reduced Import Dependence

One of the most significant trends reshaping the Australia fertilizer market is the national movement toward domestic production capacity to reduce reliance on volatile global supply chains. Australia has historically imported the majority of its fertilizer requirements, leaving the sector exposed to international price swings and logistics disruptions. This vulnerability was starkly exposed during the global supply chain crises of 2021-2023, prompting both government and private sector action. Perdaman Industries is advancing its AUD 6 billion urea-ammonium nitrate facility in Karratha, Western Australia, which will produce approximately 2.3 million tons annually when commissioned between 2025-2027. Simultaneously, Woodside Energy's Beaumont New Ammonia project is expected to add 1.1 million tons of capacity, with first production targeted for 2026. These landmark investments represent a structural shift in Australia's fertilizer supply architecture, moving from import-dependent procurement to vertically integrated domestic manufacturing. The Australian government has further supported this transition through AUD 814 million in subsidies for green ammonia production, incentivizing low-emissions nitrogen manufacturing that aligns with the country's broader climate and agricultural sustainability objectives.

Growing Adoption of Biofertilizers and Sustainable Nutrient Solutions

A second defining trend in the Australian fertilizer landscape is the accelerating adoption of biofertilizers and sustainable nutrient management solutions, driven by increasing environmental awareness, tightening regulatory requirements, and growing consumer demand for sustainably produced food. Australian regulatory authorities are imposing stricter limits on heavy metals in fertilizer products, with cadmium content limits tightening to not exceed 300 mg/kg from 2026, which is constraining supply options for conventional imports and encouraging the development of cleaner alternatives. Biofertilizers—including nitrogen-fixing bacteria, phosphate-solubilizing microorganisms, and mycorrhizal fungi formulations—are gaining market share among organic producers and progressive conventional farmers seeking to reduce chemical input costs while improving long-term soil biology and structure. The federal government's 2035 agricultural emissions-reduction plan has further accelerated adoption of low-emissions nitrogen products, with enhanced efficiency fertilizers (EEFs) featuring nitrification and urease inhibitors becoming standard recommendations from agricultural advisors across grain-growing regions. This convergence of regulatory pressure, sustainability commitments, and agronomic benefits is positioning biofertilizers and enhanced-efficiency products as a structurally growing segment within Australia's fertilizer market.

Australia Fertilizer Market Summary

• Market Size (2025): USD 2.8 Billion

• Forecast Value (2034): USD 3.9 Billion

• Growth Rate (CAGR 2026-2034): 3.43%

• Key Product Types: Chemical Fertilizers, Biofertilizers

• Primary Growth Drivers: Expanding domestic production capacity, precision agriculture adoption, government green ammonia subsidies, rising agricultural export volumes, and tightening environmental regulations

Australia Fertilizer Market Growth Drivers

Expanding Agricultural Output and Export-Oriented Production Intensification

A primary driver fueling the Australia fertilizer market is the continued expansion of agricultural output, particularly in export-oriented commodity crops. Australia's agricultural sector generated approximately USD 46 billion in exports during fiscal year 2023-24, with wheat, canola, barley, and horticultural products forming the backbone of this output. To sustain high yields and maintain soil fertility across successive growing seasons, farmers are intensifying fertilizer application—particularly nitrogenous and phosphatic products—across the major grain-growing regions of Western Australia, New South Wales, and Victoria. The growing global demand for Australian agricultural commodities, coupled with government trade agreements expanding market access in Asia-Pacific, is creating sustained upward pressure on fertilizer consumption. As broad-acre farming operations scale to meet international demand, the requirement for both bulk straight fertilizers and precision-formulated complex blends continues to rise, directly supporting the market's growth trajectory through 2034.

Government Incentives for Green Ammonia and Low-Emissions Fertilizer Manufacturing

Government policy support represents another critical growth driver for the Australian fertilizer market. The federal government has committed AUD 814 million (approximately USD 578 million) in subsidies to support domestic green ammonia production, directly reducing manufacturing costs for low-emissions nitrogen fertilizers and strengthening the economic viability of local production against cheaper imports. This policy framework aligns with Australia's 2035 agricultural emissions-reduction plan, which targets meaningful reductions in greenhouse gas output from fertilizer use across the farming sector. Beyond direct subsidies, state governments in Western Australia, Queensland, and South Australia are offering infrastructure incentives and streamlined approvals for fertilizer manufacturing and storage facilities. Agfert Fertilizers, for instance, completed a new 20,000-ton fertilizer storage and distribution facility on the Eyre Peninsula in early 2025, featuring approximately 10,000 square meters of covered storage. These combined federal and state policy mechanisms are creating a supportive ecosystem for domestic fertilizer production investment, driving both supply-side capacity expansion and demand-side adoption of next-generation sustainable fertilizer products.

Australia Fertilizer Market Segments

The Australia fertilizer market is segmented across multiple dimensions, reflecting the diverse needs of the country's agricultural sector:

• Breakup by Product Type: The market is categorized into chemical fertilizers and biofertilizers. Chemical fertilizers continue to dominate owing to their broad-acre efficiency and established supply chains, while biofertilizers are gaining traction among organic producers and environmentally conscious farming operations seeking sustainable soil management solutions.

• Breakup by Straight Fertilizer Category: Straight fertilizers are divided into nitrogenous (urea, calcium ammonium nitrate, ammonium nitrate, ammonium sulfate, anhydrous ammonia), phosphatic (MAP, DAP, SSP, TSP), potash (MoP, SoP), secondary macronutrients (calcium, magnesium, sulfur), and micronutrients (zinc, manganese, copper, iron, boron, molybdenum). Straight blends accounted for approximately 86.9% of the market in 2025, with nitrogenous products leading demand across cereal and oilseed cropping systems.

• Breakup by Product Form: The market is segmented into dry and liquid forms. Dry fertilizers remain the predominant format for bulk broad-acre application, while liquid formulations are experiencing growing adoption driven by precision agriculture technologies that enable more efficient variable-rate application across diverse soil and crop conditions.

• Breakup by Crop Type: The market segments by crop type include grains and cereals, pulses and oilseeds, fruits and vegetables, flowers and ornamentals, and others. Grains and cereals—particularly wheat, barley, and canola—constitute the largest consumption segment, reflecting Australia's position as a major global exporter of these staple commodities.

• Breakup by Region: Regional segmentation includes Australia Capital Territory and New South Wales, Victoria and Tasmania, Queensland, Northern Territory and Southern Australia, and Western Australia. Western Australia and New South Wales are the leading fertilizer-consuming regions, driven by their extensive grain and oilseed production, while Queensland contributes significant demand from sugarcane and horticultural applications.

Australia Fertilizer Market Competitive Landscape

The competitive landscape of the Australia fertilizer market features a mix of established domestic manufacturers, global chemical conglomerates, and emerging specialty fertilizer companies. Key players include Incitec Pivot Fertilisers (IPF), one of Australia's largest domestic producers with extensive manufacturing and distribution infrastructure, and Agfert Fertilizers, which has been expanding its storage and distribution capacity with new facilities on the Eyre Peninsula. The market also includes major international participants such as Nutrien, Yara International, CSBP (Wesfarmers), and Impact Fertilisers, which compete across product lines ranging from bulk commodity fertilizers to precision specialty formulations. Emerging entrants in the biofertilizer and green ammonia space are intensifying competition, with Perdaman Industries' Karratha mega-facility poised to reshape the domestic manufacturing landscape. These players are investing in advanced manufacturing technologies, expanding logistics networks, and developing sustainable product portfolios to capture market share in an increasingly quality-conscious and environmentally regulated market environment.

Latest News and Development in the Australia Fertilizer Market

• January 2025: Agfert Fertilizers completed its new 20,000-ton fertilizer storage and distribution facility on the Eyre Peninsula in South Australia, featuring approximately 10,000 square meters of covered storage structured across three major stockpiles and eight smaller storage sections, enhancing supply chain resilience for regional farmers.

• 2025: Perdaman Industries continued advancing construction on its AUD 6 billion urea-ammonium nitrate manufacturing facility in Karratha, Western Australia, which will produce approximately 2.3 million tons annually and represent the largest single fertilizer production investment in Australian history.

• 2025: The Australian government announced that cadmium content limits in imported fertilizers would tighten to not exceed 300 mg/kg from 2026, marking a significant regulatory shift that is expected to reshape import supply chains and accelerate domestic production of compliant fertilizer products.

• 2025-2026: The Australian dollar depreciated to its lowest level against the US dollar in 22 years, significantly increasing the landed cost of imported fertilizers priced in USD and strengthening the business case for domestic manufacturing and alternative sourcing strategies across the fertilizer supply chain.

• 2026: Woodside Energy's Beaumont New Ammonia project is targeting first production in 2026, adding approximately 1.1 million tons of ammonia capacity to Australia's domestic fertilizer feedstock supply and supporting the country's green hydrogen and low-emissions fertilizer manufacturing ambitions.

Note: If you require any specific information not currently covered within the scope of the report, IMARC Group will provide it as part of customization.

Speak to an analyst:

https://www.imarcgroup.com/request?type=report&id=21966&flag=E

𝗔𝗯𝗼𝘂𝘁 𝗨𝘀

IMARC Group is a global management consulting firm that helps companies in strategy, operations, technology, and mergers & acquisitions. We have been a trusted research partner for industry leaders, providing comprehensive market insights and strategic advisory services. Our extensive research network spans across 135+ countries, and we have assisted over 3,500 clients worldwide. We offer syndicated research reports, customized research solutions, and consulting services to help businesses make informed decisions and achieve their growth targets. With a team of over 500 analysts and consultants, IMARC Group is well-positioned to provide actionable insights and data-driven recommendations.

𝗖𝗼𝗻𝘁𝗮𝗰𝘁 𝗨𝘀

IMARC Group

134 N 4th St. Brooklyn, NY 11249, USA

Email: sales@imarcgroup.com

Tel No: (D) +91 120 433 0800

United States: +1-631-791-1145